In This Update: Investment Spotlight | Stock Market Review | Economic Review & Outlook

Chart of the Month | Closing Statements

INVESTMENT SPOTLIGHT

SNL Turned 50 Years Old

An estimated 15 million viewers tuned in for Saturday Night Live’s 50th Anniversary Special last month and thanks to the power of streaming, countless others did so after the fact. This is one of the benefits of living in a digital age with all of the comforts of an on-demand electronic lifestyle. Invited, but absent from the celebration was Elon Musk, who famously sent the value of his favorite cryptocurrency (internet meme-inspired Dogecoin) plummeting after referring to it as a “hustle” in a tongue-in-cheek comment on SNL’s Weekend Update in May 2021. Musk continued to capture more “DOGE” headlines than ever again last month based on his work with the Department of Government Efficiency, a non-government agency created by executive order to recommend ways to reduce government spending and waste. Also topping recent headlines was President Trump signing an executive order for the U.S. government to establish a strategic reserve of cryptocurrencies by using tokens currently owned by the government (having been forfeited to the federal government as part of criminal and civil proceedings.) This was disappointing news for crypto speculators looking for the government to be a major buyer, expecting to ride a new source of demand for the digital coins which are valued solely on supply and demand while trading outside the regulated confines of any central banking system.

MARKET INDEX RETURNS | February 2025 | YTD 2025 |

S&P 500 Index | -1.3% | 1.4% |

Russell 2000 Index | -5.4% | -2.9% |

MSCI EAFE Index | 1.9% | 7.3% |

Bloomberg US Agg. Bond Index | 2.2% | 2.7% |

FTSE 3 Mo. T-Bill Index | 0.3% | 0.7% |

“There is no such uncertainty as a sure thing.” Robert Burns, National Poet of Scotland

STOCK MARKET REVIEW & OUTLOOK

Market Volatility Took an Upturn

Despite equity markets hitting new all-time highs during the month, market volatility came in like a lamb and out like a lion in February, although in a historical context the VIX (measure of stock market volatility) merely shifted from well below average to only modestly above average, so perhaps more like a fairly disinterested lion resting comfortably in a zoo.

Information Technology stocks continued to struggle for a second month, this time joined by other growth-oriented sectors (unlike last month) with Consumer Discretionary and Communication Services suffering the largest pullbacks. The most defensive sector of the index, Consumer Staples, led for the month and similarly defensive Healthcare has been the most profitable contributor to U.S. equity portfolios thus far this year. International markets had another positive showing, increasing the lead over U.S. equity markets in 2025.

The yield on the bellwether 10-Year U.S. Treasury pulled back further during the month as risk appetite turned decidedly off. Demand for the safety of U.S. Treasuries drove prices up and yields down with the 10-Year closing the month at 4.22%. The 2-Year yield pulled back as well, but the all-important 2-10 Treasury spread remained in positive territory at 0.21%.

S&P 500 SECTOR RETURNS | February 2025 | YTD 2025 |

Communication Services | -6.3% | 2.3% |

Consumer Discretionary | -9.4% | -5.4% |

Consumer Staples | 5.7% | 7.9% |

Energy | 4.0% | 6.1% |

Financials | 1.4% | 8.0% |

Healthcare | 1.5% | 8.4% |

Industrials | -1.4% | 3.5% |

Information Technology | -1.3% | -4.2% |

Materials | 0.0% | 5.6% |

Utilities | 1.7% | 4.7% |

Real Estate | 4.2% | 6.1% |

ECONOMIC REVIEW & OUTLOOK

Inflation Readings Have Been Neither Amusing nor a Walk in the Park

Inflation readings remained stubborn and sticky, much like an overstimulated child being escorted out from a day at the amusement park by exhausted parents. The latest report of the Consumer Price Index (CPI) showed a year-on-year increase of 3%, driven higher primarily by rising food and energy prices. “Eggflation” continues to weigh on consumers with whopping year-on-year price increases north of 50%. The Core CPI, excluding volatile food and energy costs, was equally hot due to rising shelter costs. Price increases are a likely culprit to the very weak Retail Sales print released last month. A decline of 0.9% in January is the largest drop in nearly two years.

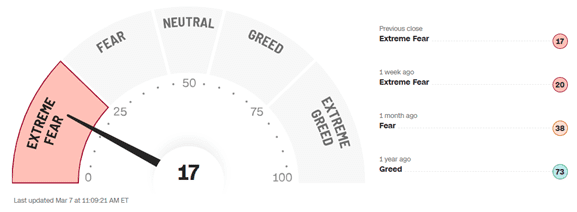

CHART OF THE MONTH

Fear & Greed Index

Source: CNN

The CNN Fear & Greed Index has quickly jumped to redline in the “Extreme Fear” category from a “Fear” reading a month ago and “Greed” a year ago. The measure incorporates a series of factors including market momentum, stock price strength and breadth, put and call options, market volatility, junk bond and safe haven demand. While the technical metrics of this measure have weakened, long-term fundamental investors understand it is merely a sign to take a deep breath and look for opportunities as others potentially overreact. As Warren Buffet said, it pays to be “fearful when others are greedy and greedy when others are fearful.”

CLOSING STATEMENT

Looking Ahead

Rest assured that we are closely monitoring recent market gyrations (so feel free to leave that to us) and find the current levels of volatility as normal as the change in seasons. Markets will chill, thaw and bloom at an unpredictable pace but much like the approaching spring, the crocus will soon pop, and the normal ebb and flow of cycles will continue.

The Atlanta Fed estimate for Gross Domestic Product (GDP) in the U.S. for the first quarter of the year now stands at negative 2.4%. If the prediction holds, it will be the first negative reading since the second quarter of 2022. In times of economic uncertainty, investors are well served to focus on the strongest, high quality, companies with solid financial strength, recurring cash flows and stable economic moats. In addition to holding the stocks and bonds of these companies, long-term investors are wise to capitalize on the overreactions of others by adding to high conviction positions at attractive valuations during usual periods of market stress.

We are fully expecting the Fed to remain on hold with any rate decisions at their next meeting on March 19th. We are of the consensus view that current reports on inflation and employment do not warrant an additional cut to the Fed Funds Rate at this time.

If you missed our primer on tariff basics in last month’s newsletter, all are welcomed to give it a read on the Resources – Newsletters tab on our website. Please reach out to one of your Account Officers or any member of our Executive Leadership Team to discuss topics raised in this letter or if we can assist you in any other way.

As always, please feel free to join the conversation on our socials – Facebook and LinkedIn!

Meet The Plimoth Investment Advisors Executive Leadership Team

Steven A. Russo, CFA

Chairman of the Board

508‑591‑6202

srusso@pliadv.com

Louis E. Sousa, CFA

President & Chief Executive Officer

508‑675‑4313

lsousa@pliadv.com

Mark J. Gendreau, CFP ®

Senior Vice President & Chief Investment Officer

508-591-6211

mgendreau@pliadv.com

Edward J. Misiolek

Senior Vice President & Operations Officer

508‑675‑4316

emisiolek@pliadv.com

Teresa A. Prue, CFP®

Senior Vice President &

Head of Fiduciary Services and Administration

508‑591‑6221

tprue@pliadv.com