In This Update: Investment Spotlight | Stock Market Review | Economic Review & Outlook

Chart of the Month | Closing Statements

INVESTMENT SPOTLIGHT

Maintain a Healthy Diet of Diversified Stock Holdings

Much like overdoing it at a pizza party, investors should be cautious about stuffing too much of a “good thing” into their portfolios. For a portfolio currently allocated with a market weight to the information technology sector (a whopping 38%) perhaps that next hot AI stock being plugged as the “must have” holding could prove to be one bite too many. Prudent investors are willing to trim big winners and exposures, with the goal of managing concentration risk. Managing a well-diversified portfolio is a key element of long-term investment success. In addition to providing exposure to multiple opportunities (that may be in or out of favor at any given time) diversified portfolios are less volatile, with fewer major swings in valuation than can often be experienced with heavily concentrated portfolios. Maintaining the proper balance between risk and return is a tried-and-true concept as old as the first stock trades that took place under a buttonwood tree in the late 1700s on Wall Street in New York City.

MARKET INDEX RETURNS | May 2026 | YTD 2026 |

S&P 500 Index | 5.3% | 11.2% |

Russell 2000 Index | 4.4% | 18.3% |

MSCI EAFE Index | 3.1% | 9.4% |

Bloomberg US Agg. Bond Index | 0.3% | 0.4% |

FTSE 3 Mo. T-Bill Index | 0.3% | 1.6% |

Law of Diminishing Marginal Utility – an economic law that states that, all else being equal, as consumption increases, the satisfaction from each additional unit consumed decreases

STOCK MARKET REVIEW & OUTLOOK

Technology Stocks for the Win… Again

Following a stellar earnings reporting season, Information Technology stocks were the hands-down winners in May as the only sector to outperform the overall S&P 500 index during the month. And outperform they did, by a factor of 3X. Robust AI infrastructure spending and investor appetite for anything semiconductor or memory related drove the flood of buy orders during the month. Semiconductor stocks (as measured by the SOX Index) had the best consecutive two months of returns in April and May (+69%) since the inception of the index, which dates back to the mid-1990s. Consumer Discretionary and Healthcare were the only other sectors in the green during the period. Energy stocks retraced some of the gains from earlier in the year as the weakest sector, driven lower by a precipitous drop in oil prices.

Major U.S. market indices catapulted to new all-time highs during the month, with the S&P 500 capping a historic run of advancing for nine consecutive weeks. Small cap stocks added to their stellar gains as well, with the Russell 2000 Index maintaining a wide margin of outperformance over the large cap S&P Index. Even the cyclically oriented Dow Jones Industrial Average reached a new milestone by surpassing 51,000 for the first time. This is a far cry from when the “old smokestack” index was celebrated for breaking into the 5-figure club in 1999 with “DOW 10,000” hats landing on the floor of the New York Stock Exchange, now historic collectors’ items.

Interest rates continued to rise across the yield curve in May. A “higher for longer” expected stance by the Federal Reserve on short-term rates and hotter than anticipated inflation readings were key drivers. The 30-Year U.S. Treasury made headlines in May (usually reserved for the 10-Year) by peaking at 5.2%..

S&P 500 SECTOR RETURNS | May 2026 | YTD 2026 |

Communication Services | -0.9% | 9.3% |

Consumer Discretionary | 2.6% | 4.1% |

Consumer Staples | -3.2% | 7.5% |

Energy | -5.6% | 26.0% |

Financials | -1.1% | -5.4% |

Healthcare | 2.5% | -3.0% |

Industrials | -0.8% | 12.0% |

Information Technology | 16.0% | 23.8% |

Materials | -0.7% | 11.9% |

Utilities | -5.1% | 4.8% |

Real Estate | -1.0% | 10.6% |

ECONOMIC REVIEW & OUTLOOK

Manufacturing is on the Move

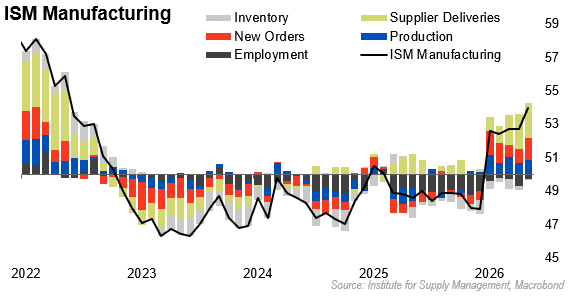

The latest reading of the ISM Manufacturing Index left even the loftiest expectations in the dust, posting the strongest results since 2022. The May report was the fifth consecutive month of expansion (a reading above 50), a remarkable shift after monthly readings in contraction since January 2025. Strong order growth and overall production were key drivers.

CHART OF THE MONTH

ISM Manufacturing Reached Levels Not Seen in Four Years

Source: ISM Manufacturing, Macrobond

CLOSING STATEMENT

Looking Ahead

The term “Middle East” was mentioned at least once in the Q1 earnings calls of 218 S&P 500 companies. Despite the concerns, corporate earnings grew remarkably by more than 28%, the highest since Q4 2021. Crude oil prices fell 19% in May, the sharpest decline since 2020, indicative of a perception of easing concerns relating to the ongoing Iran conflict. The fluidity of that situation will be a key area to watch in the coming months.

Credit card delinquencies were reported at over 13% in the first quarter of the year, the highest level since the months following the 2008 financial crisis. Disappointing results from Walmart reinforced concerns about a struggling lower-end retail consumer, further expanding the bifurcation of support from the wealthiest buyers. This is a trend worth following as a key component of economic growth.

Higher than anticipated recent inflation readings all but assure the Fed will stand pat on rates at their upcoming June 17 meeting. Probabilities from Fed Funds Futures now point to a possible rate hike (not a misprint) by year end, a potential outcome well off the radar screen at the start of the year.

AI stocks may be the flavor of the month, and there is a lot to like about their long-term prospects. They certainly deserve a place in growth investors’ portfolios, but keep in mind that bloating a portfolio full of too much of any one thing can lead to indigestion and potential remorse, much like that last “one too many” delicious slice.

Please reach out to one of your Account Officers or any member of our Executive Leadership Team to discuss topics raised in this letter or if we can assist you in any other way.

Meet The Plimoth Investment Advisors Executive Leadership Team

Steven A. Russo, CFA

Chairman of the Board

508‑591‑6202

srusso@pliadv.com

Louis E. Sousa, CFA

President & Chief Executive Officer

508‑675‑4313

lsousa@pliadv.com

Mark J. Gendreau, CFP ®

Senior Vice President & Chief Investment Officer

508-591-6211

mgendreau@pliadv.com

Edward J. Misiolek

Senior Vice President & Operations Officer

508‑675‑4316

emisiolek@pliadv.com

Teresa A. Prue, CFP®

Senior Vice President &

Head of Fiduciary Services and Administration

508‑591‑6221

tprue@pliadv.com