In This Update: Investment Spotlight | Stock Market Review | Economic Review & Outlook

Chart of the Month | Closing Statements

INVESTMENT SPOTLIGHT

Fed Governors Played Different Tunes

While the FOMC decision to stand pat on the level of interest rates was widely expected, the voting results served up another surprising takeaway. Having four dissenters in the 8-4 vote marked the most divided decision by the committee since 1992. Three members opposed the “easing bias” language in the group’s statement, and one dissented in favor of an immediate cut. The increased divergence between hawkish and dovish sentiment will keep Fed watchers anxiously awaiting any tidbit of incremental information that can be gathered during the post-meeting Governor individual press conferences extravaganza. Any hint at the potential rate path ahead should be expected to be coming soon to a headline near you.

MARKET INDEX RETURNS | April 2026 | YTD 2026 |

S&P 500 Index | 10.5% | 5.7% |

Russell 2000 Index | 12.3% | 13.3% |

MSCI EAFE Index | 7.5% | 6.1% |

Bloomberg US Agg. Bond Index | 0.1% | 0.1% |

FTSE 3 Mo. T-Bill Index | 0.3% | 1.2% |

Fed Governor Stephen Miran, to no one’s surprise, stood alone on “immediate rate cut island” during the FOMC’s April meeting.

STOCK MARKET REVIEW & OUTLOOK

Company Earnings Reports Continued to Spin the Hits

The S&P 500 charged through April with an impressive double-digit return, reaching new all-time highs. This was the strongest monthly return for the index since November 2020 and completely erased the drawdown experienced in the first quarter of the year. Investors continued to bid up stocks as earnings reports smashed expectations, all while looking through oil and gasoline price shocks, ongoing turmoil in the Middle East, and a deterioration in expectations for Fed rate accommodation coming anytime soon.

While the rally was led by technology-focused areas of the market (AI and chips in particular), six of the eleven industry sectors generated respectable positive single-digit returns alongside the stellar double-digit performance of the three most growth-oriented sectors (Communication Services, Information Technology, and Consumer Discretionary). Energy stocks reversed course during the month despite a renewed rise in oil prices, and defensive healthcare stocks were the only two S&P 500 sectors to finish the month of April in the red. Small Cap stocks were also LP record rockstars in the double-digits club, with the Russell 2000 Index hitting a new all-time high as well. International equities were solid participants in the rally, rounding out a stellar month for well-diversified equity investors.

S&P 500 SECTOR RETURNS | April 2026 | YTD 2026 |

Communication Services | 18.5% | 10.3% |

Consumer Discretionary | 11.7% | 1.5% |

Consumer Staples | 3.1% | 11.0% |

Energy | -3.5% | 33.5% |

Financials | 5.6% | -4.4% |

Healthcare | -0.4% | -5.3% |

Industrials | 7.9% | 12.9% |

Information Technology | 17.5% | 6.7% |

Materials | 2.7% | 12.7% |

Utilities | 2.1% | 10.5% |

Real Estate | 8.8% | 11.8% |

ECONOMIC REVIEW & OUTLOOK

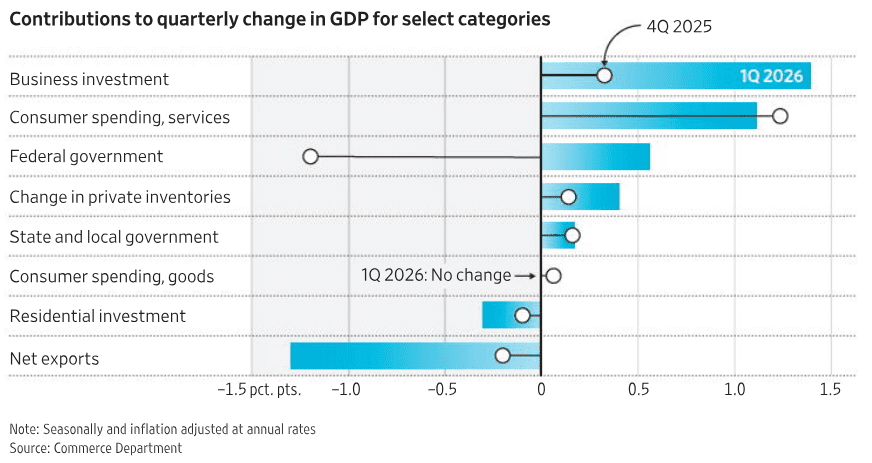

Gross Domestic Product Growth Topped the Charts in Economic News

U.S. economic growth expanded at an annualized rate of 2.0% through the end of the first quarter. The latest GDP release was buoyed by resilient services spending and a notable jump in capital investment. The expansion remains increasingly concentrated in AI-related activity, with a 17% surge in equipment purchases and a 13% increase in intellectual property spending, which is compensating for slower growth across the broader economy. Overall business investment expanded at the fastest pace in nearly three years, holding up ongoing growth despite consumer spending coming in modestly below estimates and lower than the previous quarterly reading. An increase in federal government spending was also a catalyst following the record-long government shutdown in the previous quarter.

CHART OF THE MONTH

A Surge in Business Investment Led Economic Growth

Source: Commerce Department, Wall Street Journal

CLOSING STATEMENT

Looking Ahead

Wrapping up the sixth consecutive quarter of year-on-year double-digit positive corporate earnings growth, investors will continue to have a sound basis to remain optimistic further into this equity bull run.

The labor market remains under stress with “effectively no new net creation of jobs” as Powell stated in his post meeting press conference. The 4.3% unemployment rate is low by historical standards, but job growth is weak and demand for workers has waned. We will be paying close attention to hiring, layoffs, and wage growth metrics for signs of movement from current static levels. Despite labor concerns, we expect the Fed to remain hamstrung in its ability to ease rates due to persistently sticky inflation. Futures markets are expressing a similar view with the probability of the next rate cut pushed out to the end of 2027 and odds of a dreaded hike next year rising.

Investors will be closely tuned in to the skipping record of risk involving ongoing tensions with Iran and its impact on oil prices. We will continue to synthesize the abundance of headline volume and report our key takeaways in our newly reformatted weekly market report.

Please reach out to one of your Account Officers or any member of our Executive Leadership Team to discuss topics raised in this letter or if we can assist you in any way.

Meet The Plimoth Investment Advisors Executive Leadership Team

Steven A. Russo, CFA

Chairman of the Board

508‑591‑6202

srusso@pliadv.com

Louis E. Sousa, CFA

President & Chief Executive Officer

508‑675‑4313

lsousa@pliadv.com

Mark J. Gendreau, CFP ®

Senior Vice President & Chief Investment Officer

508-591-6211

mgendreau@pliadv.com

Edward J. Misiolek

Senior Vice President & Operations Officer

508‑675‑4316

emisiolek@pliadv.com

Teresa A. Prue, CFP®

Senior Vice President &

Head of Fiduciary Services and Administration

508‑591‑6221

tprue@pliadv.com